Related Posts

Malls were amongst the hardest hit retail sectors during the peak of the pandemic. Traditional indoor malls were closed due to stay-at-home orders, and rent collections from tenants seized entirely. Anchor tenants, such as JCPenney and Nieman Marcus, filed for bankruptcy and permanently closed many stores, according to a report by CNN. Additionally, bankruptcies by major mall operators, including Washington Prime Group and CBL Properties, each of which operate more than 100 malls, negatively impacted the sector. That said, malls are bouncing back far quicker than anyone expected.

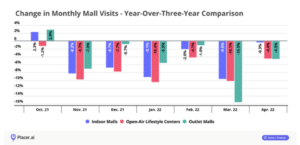

In October 2021, indoor malls saw an increase in revenue growth and foot traffic, sparking renewed hope for brick-and-mortar retail performance. Conditions downshifted, however, with the surprisingly rapid onset of the Omicron variant and a myriad of other challenges. Although traffic declines persisted into early 2022, weekly data in March, according to Placer.ai, reflected improving visit rates amidst a trend of normalizing consumer behaviors.

April’s Looking Up

Placer.ai, a leader in data science and analytics, breaks down top-performing brands for any state to understand and predict industry trends in their recently released Placer.ai 2022 Mall Index. The Index analyzes data from more than 100 top-tier indoor malls, 100 open-air lifestyle centers (excluding outlet malls) and 100 outlet malls across the country, in both urban and suburban areas.

Looking across the Index for April this year, while all mall formats still reflect an overall decline in visitors, it was much less of a contraction when compared to the previous month. Visits to the indoor mall category fell by a modest -0.3% compared to the same month in 2019, while the open-air and outlet centers segments posted a decline in traffic by -4.4% and -4.5%, respectively.

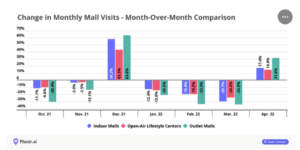

The jump in traffic becomes more apparent when analyzing visits in these three segments on a month-over-month basis. April visits rose 17.4% for indoor malls, 14.8% for open-air lifestyle centers and a notable 31.6% for outlet malls compared to March. The Easter holiday clearly provided a boost, but much of the improvement is tied as well to a growing visit normalization, especially given the initial shock of sharply rising gas prices and broad-based inflation. The former has an especially significant impact as it undermines the willingness of a consumer to travel farther for a retail experience.

Data Trending Positively Once Again

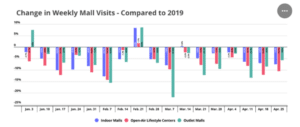

Weekly data also indicates that there is room for continued improvement. While April was the strongest month yet in 2022 for indoor malls, open-air centers, and outlet malls, these venues remain under pressure and face new challenges borne of the pandemic, compared to 2019. Improving visit gaps for open air lifestyle centers and outlet malls in the latter part of April highlights the prospect of a growing appetite for a longer trip to ensure a value-oriented or single-location retail and entertainment experience.

And the timing here is critical. While the relative strength shown in recent months is impressive, especially considering the external pressures, the summer season presents a uniquely powerful opportunity for top tier centers across all categories.

Should the wider COVID recovery continue and the impact of some of retail’s newer challenges begin to dissipate, the coming months could see a sharp rise in mall traffic and consumer engagement.