Related Posts

In a reversal from sentiment at the beginning of this year, investors are becoming increasingly bearish about the commercial real estate market. Faced with an economic slowdown, inflation, rising interest rates, supply chain issues, labor shortages and the threat of a recession, investors and capital providers to take a step back and reassess their strategies as this year concludes and the next begins.

The overarching feeling among CRE investors these days is cautious optimism—a term not unfamiliar to the industry. There are several factors behind the restrained optimism, such as the level of capital targeting commercial real estate and the sector’s ability to deliver steady yield and outpace alternative investment options.

That optimism applies more to the sector’s long-term prospects, though, with almost 70 percent of participants in the latest LightBox Investor Sentiment survey either concerned or bearish about the commercial estate market for the balance of 2022. When queried on their feelings about 2023, that figure dropped slightly to 58 percent.

For the time being, uncertainty is having a negative effect on deal volumes, pricing and the availability of capital. Investors identified inflation and supply chain disruptions as major threats to commercial real estate, with interest rates rounding out the top three. Despite predictions that the Fed will ease up on further rate hikes, investment professionals remain worried that the Fed’s efforts to tamp down inflation will instead trigger one. The vast majority (90 percent) are concerned about a looming recession, with a 56 percent saying they were “very concerned.” Just 10 percent said they weren’t concerned at all about a potential recession.

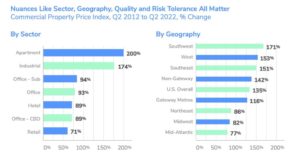

Among property types, investors are unsurprisingly more confident about some sectors than others. Sky-high demand has been driving the industrial sector for several quarters, and this trend is expected to continue, albeit not at such a frenetic pace. Industrial vacancies are hovering around 3% and lower in high-demand areas, and rents are expected to increase by 22% over the year.

There simply isn’t enough industrial stock, existing and under development, to meet demand. Citing data from ProLogis, Lightbox noted that there’s only about 375 million square feet under development in the face of 800-million-plus square feet of pent-up incremental demand. The low-risk, inflation-resistant industrial sector, with its consistently rising values, high demand and limited supply, will continue to remain in high demand for investors. And as construction costs and labor shortages put pressure on ecommerce growth, multi-story facilities and robotics will be the wave of the future.

With businesses across the country still working out their return-to-work policies, the outlook for the office sector is less positive. Since each company has a different approach, it will take a few years for a sense of normalcy to return. For now, it looks like most employers will retain some semblance of remote work; about half of companies queried in JLL’s Future of Work Survey said they plan on investing in flexible space in the coming few years.

Uncertain economic prospects are also slowing hiring decisions among commercial real estate organizations, reflecting a broader slowdown in employment trends across the country. Eight out of every 10 respondents to the Lightbox survey indicated that recent market changes have impacted hiring plans. While 20% are continuing to hire aggressively, the same share put hiring plans on hold until there is greater economic clarity. The majority, 40%, are hiring for high-priority needs, while 7% are reducing staffing.

As we transition into a new year, all of the concerns mentioned above will remain top-of-mind as the market works its way through the impact of higher interest rates and pricing adjustments. Only then will major moves likely be made.